Applied

Solution 8:

(a) Perform linear regression on auto data with mpg as response and horsepower as the predictor and display the summary results.

import statsmodels.api as sm

X = sm.add_constant(auto[['horsepower']], prepend=True)

model = sm.OLS(auto['mpg'], X)

result = model.fit()

print(result.summary())

print("Prediction for horsepower 98: " +str(result.predict([1, 98])))

print("95% CI: " +str(result.conf_int(alpha=0.05, cols=None)))

OLS Regression Results

==============================================================================

Dep. Variable: mpg R-squared: 0.606

Model: OLS Adj. R-squared: 0.605

Method: Least Squares F-statistic: 599.7

Date: Thu, 06 Sep 2018 Prob (F-statistic): 7.03e-81

Time: 21:37:43 Log-Likelihood: -1178.7

No. Observations: 392 AIC: 2361.

Df Residuals: 390 BIC: 2369.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 39.9359 0.717 55.660 0.000 38.525 41.347

horsepower -0.1578 0.006 -24.489 0.000 -0.171 -0.145

==============================================================================

Omnibus: 16.432 Durbin-Watson: 0.920

Prob(Omnibus): 0.000 Jarque-Bera (JB): 17.305

Skew: 0.492 Prob(JB): 0.000175

Kurtosis: 3.299 Cond. No. 322.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Prediction for horsepower 98: [24.46707715]

95% CI: 0 1

const 38.525212 41.346510

horsepower -0.170517 -0.145172

i. Is there a relationship between the predictor and the response?

Yes

ii. How strong is the relationship between the predictor and the response?

As the value of $R^2$-statistic is 0.606, which means that 60% variability is explained by the model.

iii. Is the relationship between the predictor and the response positive or negative?

Negative coefficient denotes negative relationship.

iv. What is the predicted mpg associated with a horsepower of 98? What are the associated 95% confidence and prediction intervals?

The value of mpg for horsepower = 98 is 24.4671.

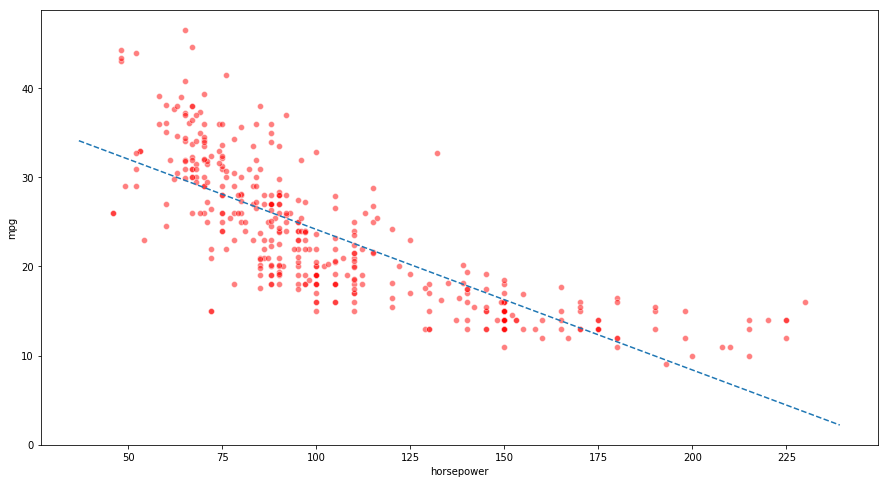

(b) Plot the response and the predictor. Also show the regression line.

import matplotlib.pyplot as plt

import numpy as np

fig = plt.figure(figsize=(15,8))

ax = fig.add_subplot(111)

ax = sns.scatterplot(x="horsepower", y="mpg", color='r', alpha=0.5, data=auto)

x_vals = np.array(ax.get_xlim())

y_vals = 39.9359 - 0.1578 * x_vals

plt.plot(x_vals, y_vals, '--')

[<matplotlib.lines.Line2D at 0x11a222048>]

Solution 9:

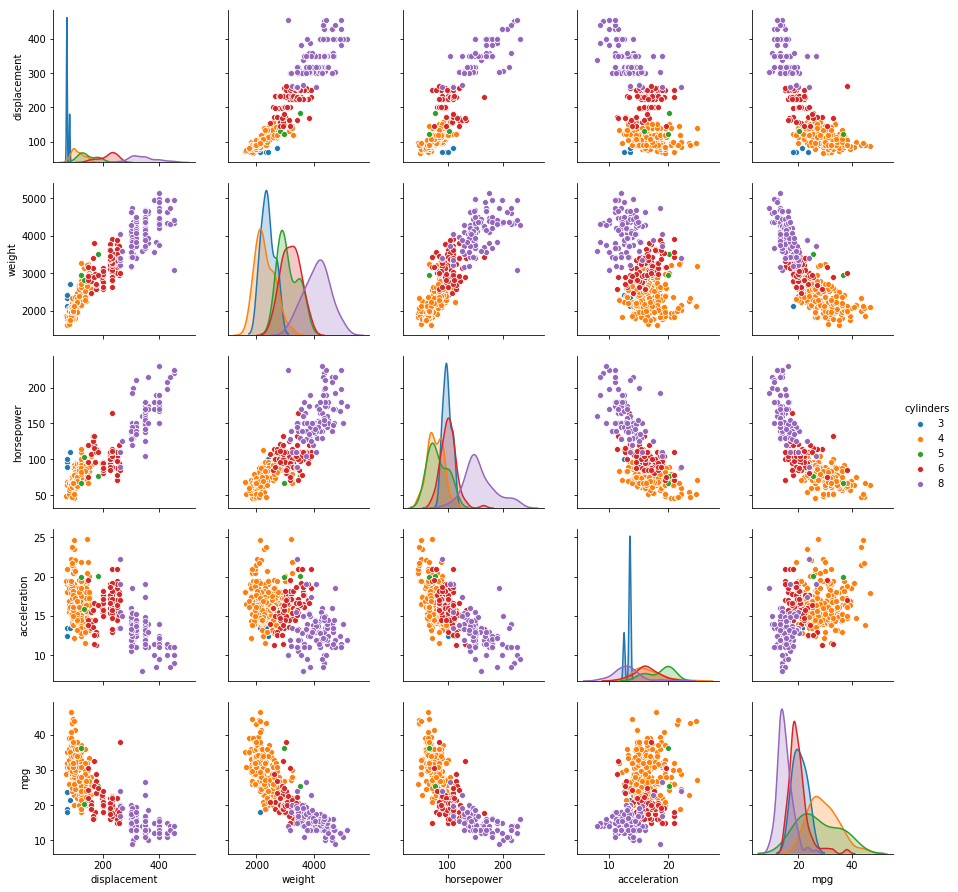

(a) Produce a scatterplot matrix which includes all of the variables in the data set.

# Scatter plot of quantitative variables

sns.pairplot(auto, vars=['displacement', 'weight', 'horsepower', 'acceleration', 'mpg'], hue='cylinders')

/Users/amitrajan/Desktop/PythonVirtualEnv/Python3_VirtualEnv/lib/python3.6/site-packages/scipy/stats/stats.py:1713: FutureWarning: Using a non-tuple sequence for multidimensional indexing is deprecated; use `arr[tuple(seq)]` instead of `arr[seq]`. In the future this will be interpreted as an array index, `arr[np.array(seq)]`, which will result either in an error or a different result.

return np.add.reduce(sorted[indexer] * weights, axis=axis) / sumval

<seaborn.axisgrid.PairGrid at 0x11a1c4f98>

(b) Compute the matrix of correlations between the variables.

auto.corr()

| mpg | cylinders | displacement | horsepower | weight | acceleration | year | origin | |

|---|---|---|---|---|---|---|---|---|

| mpg | 1.000000 | -0.777618 | -0.805127 | -0.778427 | -0.832244 | 0.423329 | 0.580541 | 0.565209 |

| cylinders | -0.777618 | 1.000000 | 0.950823 | 0.842983 | 0.897527 | -0.504683 | -0.345647 | -0.568932 |

| displacement | -0.805127 | 0.950823 | 1.000000 | 0.897257 | 0.932994 | -0.543800 | -0.369855 | -0.614535 |

| horsepower | -0.778427 | 0.842983 | 0.897257 | 1.000000 | 0.864538 | -0.689196 | -0.416361 | -0.455171 |

| weight | -0.832244 | 0.897527 | 0.932994 | 0.864538 | 1.000000 | -0.416839 | -0.309120 | -0.585005 |

| acceleration | 0.423329 | -0.504683 | -0.543800 | -0.689196 | -0.416839 | 1.000000 | 0.290316 | 0.212746 |

| year | 0.580541 | -0.345647 | -0.369855 | -0.416361 | -0.309120 | 0.290316 | 1.000000 | 0.181528 |

| origin | 0.565209 | -0.568932 | -0.614535 | -0.455171 | -0.585005 | 0.212746 | 0.181528 | 1.000000 |

(c) Perform a multiple linear regression with mpg as the response and all other variables except name as the predictors.

X = auto[['cylinders', 'displacement', 'horsepower', 'weight', 'acceleration', 'year', 'origin']]

X = sm.add_constant(X, prepend=True)

y = auto['mpg']

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: mpg R-squared: 0.821

Model: OLS Adj. R-squared: 0.818

Method: Least Squares F-statistic: 252.4

Date: Mon, 10 Sep 2018 Prob (F-statistic): 2.04e-139

Time: 19:11:35 Log-Likelihood: -1023.5

No. Observations: 392 AIC: 2063.

Df Residuals: 384 BIC: 2095.

Df Model: 7

Covariance Type: nonrobust

================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------

const -17.2184 4.644 -3.707 0.000 -26.350 -8.087

cylinders -0.4934 0.323 -1.526 0.128 -1.129 0.142

displacement 0.0199 0.008 2.647 0.008 0.005 0.035

horsepower -0.0170 0.014 -1.230 0.220 -0.044 0.010

weight -0.0065 0.001 -9.929 0.000 -0.008 -0.005

acceleration 0.0806 0.099 0.815 0.415 -0.114 0.275

year 0.7508 0.051 14.729 0.000 0.651 0.851

origin 1.4261 0.278 5.127 0.000 0.879 1.973

==============================================================================

Omnibus: 31.906 Durbin-Watson: 1.309

Prob(Omnibus): 0.000 Jarque-Bera (JB): 53.100

Skew: 0.529 Prob(JB): 2.95e-12

Kurtosis: 4.460 Cond. No. 8.59e+04

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 8.59e+04. This might indicate that there are

strong multicollinearity or other numerical problems.

i. Is there a relationship between the predictors and the response?

As the $R^2$-statistic is 0.821, we can say that 82% variability is explained by the model.

ii. Which predictors appear to have a statistically significant relationship to the response?

The predictors that have statistically significant relationship to the response are: displacement, weight, year and origin.

iii. What does the coefficient for the year variable suggest?

The coefficient of year varaible suggests that if all the other predictors are kept constant, increase of 1 in year results in 0.7508 increase in mpg.

(e) Fit linear regression models with interaction effects. Do any interactions appear to be statistically significant?

auto['cylinders_displacement'] = auto['cylinders']*auto['displacement']

auto['horsepower_displacement'] = auto['horsepower']*auto['displacement']

auto['weight_displacement'] = auto['weight']*auto['displacement']

X = auto[['cylinders', 'displacement', 'horsepower', 'weight', 'acceleration', 'year', 'origin',

'cylinders_displacement', 'horsepower_displacement', 'weight_displacement']]

X = sm.add_constant(X, prepend=True)

y = auto['mpg']

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: mpg R-squared: 0.866

Model: OLS Adj. R-squared: 0.862

Method: Least Squares F-statistic: 246.0

Date: Thu, 06 Sep 2018 Prob (F-statistic): 1.96e-159

Time: 21:37:48 Log-Likelihood: -967.41

No. Observations: 392 AIC: 1957.

Df Residuals: 381 BIC: 2000.

Df Model: 10

Covariance Type: nonrobust

===========================================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------------------

const -2.4166 4.438 -0.545 0.586 -11.142 6.309

cylinders 0.8214 0.618 1.329 0.185 -0.394 2.037

displacement -0.0778 0.013 -5.822 0.000 -0.104 -0.052

horsepower -0.1488 0.029 -5.222 0.000 -0.205 -0.093

weight -0.0062 0.001 -4.443 0.000 -0.009 -0.003

acceleration -0.1312 0.097 -1.357 0.175 -0.321 0.059

year 0.7566 0.045 16.822 0.000 0.668 0.845

origin 0.5797 0.258 2.247 0.025 0.072 1.087

cylinders_displacement -0.0014 0.003 -0.516 0.606 -0.007 0.004

horsepower_displacement 0.0004 8.27e-05 4.481 0.000 0.000 0.001

weight_displacement 1.046e-05 4.37e-06 2.393 0.017 1.87e-06 1.9e-05

==============================================================================

Omnibus: 47.260 Durbin-Watson: 1.507

Prob(Omnibus): 0.000 Jarque-Bera (JB): 97.455

Skew: 0.662 Prob(JB): 6.89e-22

Kurtosis: 5.053 Cond. No. 2.56e+07

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 2.56e+07. This might indicate that there are

strong multicollinearity or other numerical problems.

Interactions of horsepower and displacement and weight and displacement have significant effect.

Solution 10: This question should be answered using the Carseats data set.

(a) Fit a multiple regression model to predict Sales using Price, Urban, and US.

carsets = pd.read_csv("data/Carsets.csv")

carsets['US'] = carsets['US'].map({'Yes': 1, 'No': 0})

carsets['Urban'] = carsets['Urban'].map({'Yes': 1, 'No': 0})

X = carsets[['Price', 'Urban', 'US']]

X = sm.add_constant(X, prepend=True)

y = carsets['Sales']

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Sales R-squared: 0.239

Model: OLS Adj. R-squared: 0.234

Method: Least Squares F-statistic: 41.52

Date: Thu, 06 Sep 2018 Prob (F-statistic): 2.39e-23

Time: 21:37:48 Log-Likelihood: -927.66

No. Observations: 400 AIC: 1863.

Df Residuals: 396 BIC: 1879.

Df Model: 3

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 13.0435 0.651 20.036 0.000 11.764 14.323

Price -0.0545 0.005 -10.389 0.000 -0.065 -0.044

Urban -0.0219 0.272 -0.081 0.936 -0.556 0.512

US 1.2006 0.259 4.635 0.000 0.691 1.710

==============================================================================

Omnibus: 0.676 Durbin-Watson: 1.912

Prob(Omnibus): 0.713 Jarque-Bera (JB): 0.758

Skew: 0.093 Prob(JB): 0.684

Kurtosis: 2.897 Cond. No. 628.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

(b) Provide an interpretation of each coefficient in the model. Be careful—some of the variables in the model are qualitative!

Sales decreases by 0.0545 per unit increase in Price given that all the other predictors are not changed. Urban has no significant effect on the response. If all the other predictors are constant, being a US car increases the Sales by average of 1.2006.

(c) Write out the model in equation form, being careful to handle the qualitative variables properly.

The model in equation form is as follows:

$$Sales = 13.0435 - 0.0545 \times Price + 1.2006 - 0.0219 \ (if \ US, Urban)$$ $$Sales = 13.0435 - 0.0545 \times Price + 1.2006 \ (if \ US, \ not \ Urban)$$ $$Sales = 13.0435 - 0.0545 \times Price - 0.0219 \ (if \ not \ US, Urban)$$ $$Sales = 13.0435 - 0.0545 \times Price \ (if \ not \ US, not \ Urban)$$

(d) For which of the predictors can you reject the null hypothesis H0 : βj = 0?

We can reject the null hypothesis for Price and US.

(e) On the basis of your response to the previous question, fit a smaller model that only uses the predictors for which there is evidence of association with the outcome.

X = carsets[['Price', 'US']]

X = sm.add_constant(X, prepend=True)

y = carsets['Sales']

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Sales R-squared: 0.239

Model: OLS Adj. R-squared: 0.235

Method: Least Squares F-statistic: 62.43

Date: Thu, 06 Sep 2018 Prob (F-statistic): 2.66e-24

Time: 21:37:48 Log-Likelihood: -927.66

No. Observations: 400 AIC: 1861.

Df Residuals: 397 BIC: 1873.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 13.0308 0.631 20.652 0.000 11.790 14.271

Price -0.0545 0.005 -10.416 0.000 -0.065 -0.044

US 1.1996 0.258 4.641 0.000 0.692 1.708

==============================================================================

Omnibus: 0.666 Durbin-Watson: 1.912

Prob(Omnibus): 0.717 Jarque-Bera (JB): 0.749

Skew: 0.092 Prob(JB): 0.688

Kurtosis: 2.895 Cond. No. 607.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

(f) How well do the models in (a) and (e) fit the data?

If we see the $R^2$-statistic of the models, for both the models, it has a value of 0.239. Hence both the models explains 23.9% variability in data and model in (a), which has one more predictor does not improve over accuracy.

(g) Using the model from (e), obtain 95% confidence intervals for the coefficient(s).

The 95% confidence intervals for the coefficients are:

- Intercept : [11.7688, 14.2928]

- Price : [-0.0555, 0.0535]

- US : [0.6836, 1.7156]

Solution 11. In this problem we will investigate the t-statistic for the null hypothesis H0 : β = 0 in simple linear regression without an intercept. To begin, we generate a predictor x and a response y as:

import random

random.seed(1)

x = np.random.normal(loc=0, scale=1, size=100)

y = 2*x + np.random.normal(loc=0, scale=1, size=100)

(a) Perform a simple linear regression of y onto x, without an intercept. Report the coefficient estimate $\widehat{\beta}$, the standard error of this coefficient estimate, and the t-statistic and p-value associated with the null hypothesis H0 : β = 0. Comment on these results.

model = sm.OLS(y, x)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.765

Model: OLS Adj. R-squared: 0.763

Method: Least Squares F-statistic: 322.1

Date: Thu, 06 Sep 2018 Prob (F-statistic): 6.90e-33

Time: 21:37:48 Log-Likelihood: -136.69

No. Observations: 100 AIC: 275.4

Df Residuals: 99 BIC: 278.0

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 1.8076 0.101 17.946 0.000 1.608 2.007

==============================================================================

Omnibus: 0.587 Durbin-Watson: 1.969

Prob(Omnibus): 0.746 Jarque-Bera (JB): 0.714

Skew: -0.083 Prob(JB): 0.700

Kurtosis: 2.620 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Coefficient estimate is 1.9766 with a standard error of 0.099. The t-statistic associated with null hypothesis is 19.900 which gives a significantly low p-value. The $R^2$-statistic, whose value is 0.800, suggests that the predictor is significant and explains 80% of the variability.

(b) Now perform a simple linear regression of x onto y without an intercept, and report the coefficient estimate, its standard error, and the corresponding t-statistic and p-values associated with the null hypothesis H0 : β = 0. Comment on these results.

model = sm.OLS(x, y)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.765

Model: OLS Adj. R-squared: 0.763

Method: Least Squares F-statistic: 322.1

Date: Thu, 06 Sep 2018 Prob (F-statistic): 6.90e-33

Time: 21:37:48 Log-Likelihood: -64.089

No. Observations: 100 AIC: 130.2

Df Residuals: 99 BIC: 132.8

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 0.4232 0.024 17.946 0.000 0.376 0.470

==============================================================================

Omnibus: 0.724 Durbin-Watson: 1.990

Prob(Omnibus): 0.696 Jarque-Bera (JB): 0.841

Skew: 0.179 Prob(JB): 0.657

Kurtosis: 2.729 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Coefficient estimate is 0.4048 with a standard error of 0.020. The t-statistic associated with null hypothesis is 19.900 which gives a significantly low p-value. The $R^2$-statistic, whose value is 0.800, suggests that the predictor is significant and explains 80% of the variability.

(c) What is the relationship between the results obtained in (a) and (b)?

The coefficients for the two models follow inverse relationship. The t-statistic and $R^2$-statistic are same.

Solution 12: This problem involves simple linear regression without an intercept.

(a) Recall that the coefficient estimate $\widehat{\beta}$ for the linear regression of Y onto X without an intercept is given by:

$$\widehat{\beta} = \frac{\sum _{i=1}^{n}x_i y_i}{\sum _{i^{’}=1}^{n}x _{i^{’}}^2}$$

Under what circumstance is the coefficient estimate for the regression of X onto Y the same as the coefficient estimate for the regression of Y onto X?

The coefficients will be same when:

$$\sum _{i=1}^{n}x _{i}^2 = \sum _{i=1}^{n}y _{i}^2$$

(c) Generate an example with n = 100 observations in which the coefficient estimate for the regression of X onto Y is the same as the coefficient estimate for the regression of Y onto X.

random.seed(1)

x = np.random.normal(loc=0, scale=1, size=100)

y = np.random.normal(loc=0, scale=1, size=100)

print(np.sum(x**2))

print(np.sum(y**2))

model = sm.OLS(y, x)

result = model.fit()

print(result.summary())

print("\n \n")

model = sm.OLS(x, y)

result = model.fit()

print(result.summary())

83.09270311310463

121.64942659232169

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.000

Model: OLS Adj. R-squared: -0.010

Method: Least Squares F-statistic: 0.004235

Date: Thu, 06 Sep 2018 Prob (F-statistic): 0.948

Time: 21:37:48 Log-Likelihood: -151.69

No. Observations: 100 AIC: 305.4

Df Residuals: 99 BIC: 308.0

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 -0.0079 0.122 -0.065 0.948 -0.249 0.233

==============================================================================

Omnibus: 2.389 Durbin-Watson: 1.875

Prob(Omnibus): 0.303 Jarque-Bera (JB): 1.867

Skew: -0.319 Prob(JB): 0.393

Kurtosis: 3.205 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.000

Model: OLS Adj. R-squared: -0.010

Method: Least Squares F-statistic: 0.004235

Date: Thu, 06 Sep 2018 Prob (F-statistic): 0.948

Time: 21:37:48 Log-Likelihood: -132.63

No. Observations: 100 AIC: 267.3

Df Residuals: 99 BIC: 269.9

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

x1 -0.0054 0.083 -0.065 0.948 -0.170 0.159

==============================================================================

Omnibus: 5.314 Durbin-Watson: 1.818

Prob(Omnibus): 0.070 Jarque-Bera (JB): 5.119

Skew: 0.554 Prob(JB): 0.0773

Kurtosis: 3.012 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Solution 13: In this exercise you will create some simulated data and will fit simple linear regression models to it. Make sure to use set.seed(1) prior to starting part (a) to ensure consistent results.

random.seed(1)

(a) Create a vector, x, containing 100 observations drawn from a N(0, 1) distribution. This represents a feature, X.

X = np.random.normal(loc=0, scale=1, size=100)

(b) Create a vector, eps, containing 100 observations drawn from a N(0, 0.25) distribution i.e. a normal distribution with mean zero and variance 0.25.

eps = np.random.normal(loc=0, scale=0.25, size=100)

(c) Using X and eps, generate a vector y according to the model $Y = −1 + 0.5X + \epsilon$. What is the length of the vector Y? What are the values of β0 and β1 in this linear model?

Y = -1 + (0.5*X) + eps

print("Length of Y:" +str(len(Y)))

Length of Y:100

Lengt of Y is 100. The values of $\beta_0$ and $\beta_1$ are -1 and 0.5 respectively.

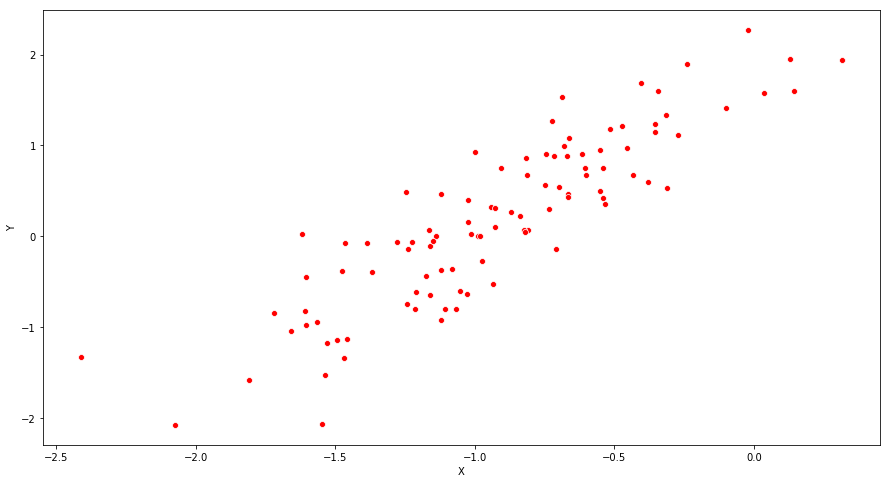

(d) Create a scatterplot displaying the relationship between x and y. Comment on what you observe.

fig = plt.figure(figsize=(15,8))

ax = fig.add_subplot(111)

ax = sns.scatterplot(Y, X, color='r')

ax.set_xlabel("X")

ax.set_ylabel("Y")

plt.show()

(e) Fit a least squares linear model to predict y using x. Comment on the model obtained. How do $\widehat{\beta_0}$ and $\widehat{\beta_1}$ compare to β0 and β1?

The values of $\widehat\beta_0$ and $\widehat\beta_1$ are -1.0145 and 0.5130 respectively. They are quite similar to $\beta_0$ and $\beta_1$.

X_1 = sm.add_constant(X, prepend=True)

model = sm.OLS(Y, X_1)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.772

Model: OLS Adj. R-squared: 0.770

Method: Least Squares F-statistic: 332.6

Date: Thu, 06 Sep 2018 Prob (F-statistic): 2.89e-33

Time: 21:37:49 Log-Likelihood: 3.2646

No. Observations: 100 AIC: -2.529

Df Residuals: 98 BIC: 2.681

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -1.0103 0.024 -41.824 0.000 -1.058 -0.962

x1 0.4691 0.026 18.237 0.000 0.418 0.520

==============================================================================

Omnibus: 4.700 Durbin-Watson: 2.124

Prob(Omnibus): 0.095 Jarque-Bera (JB): 4.057

Skew: -0.464 Prob(JB): 0.132

Kurtosis: 3.336 Cond. No. 1.24

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

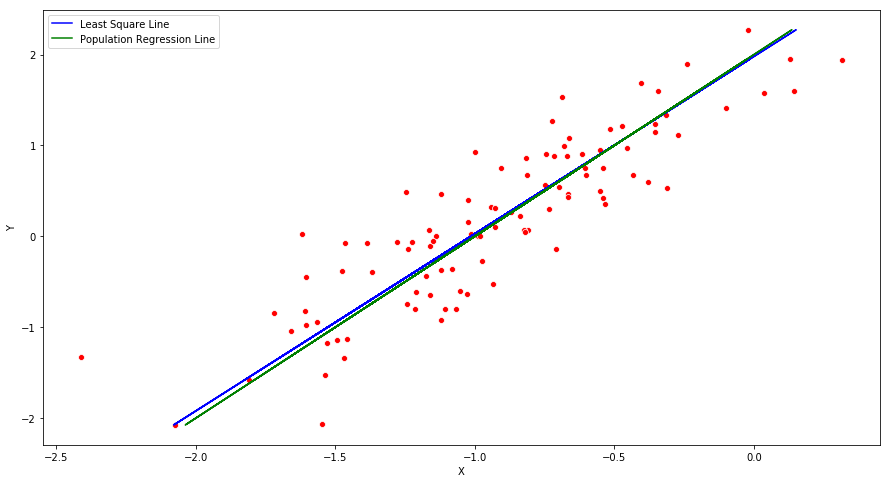

(f) Display the least squares line on the scatterplot obtained in (d). Draw the population regression line on the plot, in a different color. Use the legend() command to create an appropriate legend.

fig = plt.figure(figsize=(15,8))

ax = fig.add_subplot(111)

ax = sns.scatterplot(Y, X, color='r')

y_hat = -1.0145 + (0.5130 * X)

plt.plot(y_hat, X, color='blue', label="Least Square Line")

y_population = -1 + (0.5 * X)

plt.plot(y_population, X, color='green', label="Population Regression Line")

ax.set_xlabel("X")

ax.set_ylabel("Y")

ax.legend()

plt.show()

(g) Now fit a polynomial regression model that predicts y using x and $x^2$. Is there evidence that the quadratic term improves the model fit? Explain your answer.

As the p-value for the predictor $x^2$ is 0.644, it is not significant. The $R^2$-statistic has not improved much as well.

X_2 = X**2

X_pol = np.stack((X, X_2), axis=-1)

X_pol = sm.add_constant(X_pol, prepend=True)

model = sm.OLS(Y, X_pol)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.775

Model: OLS Adj. R-squared: 0.770

Method: Least Squares F-statistic: 167.1

Date: Thu, 06 Sep 2018 Prob (F-statistic): 3.73e-32

Time: 21:37:49 Log-Likelihood: 3.8606

No. Observations: 100 AIC: -1.721

Df Residuals: 97 BIC: 6.094

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -1.0301 0.030 -33.950 0.000 -1.090 -0.970

x1 0.4630 0.026 17.592 0.000 0.411 0.515

x2 0.0238 0.022 1.078 0.283 -0.020 0.068

==============================================================================

Omnibus: 5.916 Durbin-Watson: 2.203

Prob(Omnibus): 0.052 Jarque-Bera (JB): 5.290

Skew: -0.522 Prob(JB): 0.0710

Kurtosis: 3.424 Cond. No. 2.33

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Solution 14: This problem focuses on the collinearity problem.

(a) Generate data by following R command:

- set .seed (1)

- x1=runif (100)

- x2 =0.5* x1+rnorm (100) /10

- y=2+2* x1 +0.3* x2+rnorm (100)

The last line corresponds to creating a linear model in which y is a function of x1 and x2. Write out the form of the linear model. What are the regression coefficients?

The linear model is:

$$ Y = 2 + 2 \times X1 + 0.3 \times X2 + \epsilon$$

The regression coefficients are 2,2 and 0.3.

random.seed(1)

X1 = np.random.normal(loc=0, scale=1, size=100)

X2 = 0.5*X1 + (np.random.normal(loc=0, scale=1, size=100)/10)

Y = 2 + (2*X1) + (0.3*X2) + (np.random.normal(loc=0, scale=1, size=100))

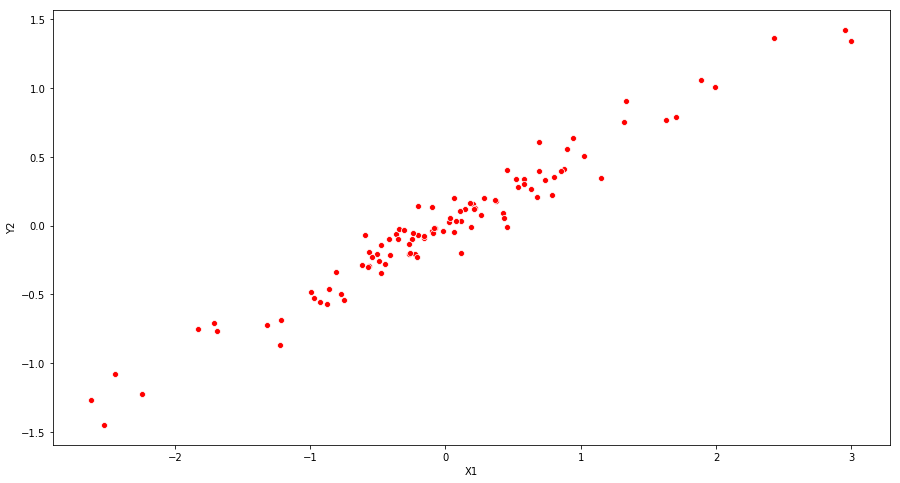

(b) What is the correlation between X1 and X2? Create a scatterplot displaying the relationship between the variables.

The correlation coefficient between X1 and X2 is 0.9836387796085876. The scatterplot shows the same tendency.

print("Correlation coefficient: " + str(np.corrcoef(X1, X2)[0][1]))

fig = plt.figure(figsize=(15,8))

ax = fig.add_subplot(111)

ax = sns.scatterplot(x=X1, y=X2, color='r')

ax.set_xlabel("X1")

ax.set_ylabel("Y2")

plt.show()

Correlation coefficient: 0.9773524295882932

(c) Using this data, fit a least squares regression to predict y using x1 and x2. Describe the results obtained. What are $\widehat{\beta_0}, \widehat{\beta_1}, \widehat{\beta_2}$? How do these relate to the true β0, β1, and β2? Can you reject the null hypothesis H0 : β1 = 0? How about the null hypothesis H0 : β2 = 0?

The values of $\widehat{\beta_0}, \widehat{\beta_1}, \widehat{\beta_2}$ are 1.8824, 1.1253 and 2.0781. We can reject the null hypothesis for $\widehat{\beta_0}$ and $\widehat{\beta_1}$ as p-values are less than 0.05. If we increase the level of confidence to 0.01, the null hypothesis for $\widehat{\beta_1}$ can not be rejected.

X = np.stack((X1, X2), axis=-1)

X = sm.add_constant(X, prepend=True)

model = sm.OLS(Y, X)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.841

Model: OLS Adj. R-squared: 0.837

Method: Least Squares F-statistic: 255.6

Date: Thu, 06 Sep 2018 Prob (F-statistic): 2.15e-39

Time: 21:37:49 Log-Likelihood: -137.49

No. Observations: 100 AIC: 281.0

Df Residuals: 97 BIC: 288.8

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 2.0716 0.097 21.300 0.000 1.879 2.265

x1 1.8083 0.457 3.956 0.000 0.901 2.716

x2 0.7538 0.893 0.845 0.400 -1.018 2.525

==============================================================================

Omnibus: 0.011 Durbin-Watson: 2.033

Prob(Omnibus): 0.995 Jarque-Bera (JB): 0.108

Skew: 0.021 Prob(JB): 0.947

Kurtosis: 2.844 Cond. No. 11.6

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

(d) Now fit a least squares regression to predict y using only x1. Comment on your results. Can you reject the null hypothesis H0 : β1 = 0?

The values of $\widehat{\beta_0}$ and $\widehat{\beta_1}$ are 1.8988 and 2.1601. We can reject the null hypothesis for $\widehat{\beta_1}$ as p-value is very low.

X = sm.add_constant(X1, prepend=True)

model = sm.OLS(Y, X)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.839

Model: OLS Adj. R-squared: 0.838

Method: Least Squares F-statistic: 512.0

Date: Thu, 06 Sep 2018 Prob (F-statistic): 1.07e-40

Time: 21:37:49 Log-Likelihood: -137.85

No. Observations: 100 AIC: 279.7

Df Residuals: 98 BIC: 284.9

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 2.0752 0.097 21.390 0.000 1.883 2.268

x1 2.1856 0.097 22.628 0.000 1.994 2.377

==============================================================================

Omnibus: 0.020 Durbin-Watson: 1.985

Prob(Omnibus): 0.990 Jarque-Bera (JB): 0.152

Skew: -0.009 Prob(JB): 0.927

Kurtosis: 2.810 Cond. No. 1.01

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

(e) Now fit a least squares regression to predict y using only x2. Comment on your results. Can you reject the null hypothesis H0 : β1 = 0?

The values of $\widehat{\beta_0}$ and $\widehat{\beta_1}$ are 1.8606 and 4.2647. We can reject the null hypothesis for $\widehat{\beta_1}$ as p-value is very low.

X = sm.add_constant(X2, prepend=True)

model = sm.OLS(Y, X)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.815

Model: OLS Adj. R-squared: 0.813

Method: Least Squares F-statistic: 431.1

Date: Thu, 06 Sep 2018 Prob (F-statistic): 1.16e-37

Time: 21:37:49 Log-Likelihood: -144.97

No. Observations: 100 AIC: 293.9

Df Residuals: 98 BIC: 299.1

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 2.0543 0.104 19.721 0.000 1.848 2.261

x1 4.2050 0.203 20.764 0.000 3.803 4.607

==============================================================================

Omnibus: 0.125 Durbin-Watson: 2.209

Prob(Omnibus): 0.939 Jarque-Bera (JB): 0.188

Skew: 0.081 Prob(JB): 0.910

Kurtosis: 2.864 Cond. No. 1.94

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

(f) Do the results obtained in (c)–(e) contradict each other? Explain your answer.

In case of collinearity, t-statistic declines and consequently we may fail to reject the null hypothesis. This is the case for $\widehat{\beta_2}$ in (c). For the model in (c), the standard errors corresponding to $\beta$s are high and hence the t-statistic does not capture the accurate behaviour.

Solution 15: This problem involves the Boston data set, which we saw in the lab for this chapter. We will now try to predict per capita crime rate using the other variables in this data set. In other words, per capita crime rate is the response, and the other variables are the predictors.

from sklearn.datasets import load_boston

boston = load_boston()

df_boston = pd.DataFrame(boston.data, columns=['CRIM', 'ZN', 'INDUS', 'CHAS', 'NOX', 'RM', 'AGE', 'DIS', 'RAD', 'TAX',

'PTRATIO', 'B', 'LSTAT'])

df_boston.head()

| CRIM | ZN | INDUS | CHAS | NOX | RM | AGE | DIS | RAD | TAX | PTRATIO | B | LSTAT | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.00632 | 18.0 | 2.31 | 0.0 | 0.538 | 6.575 | 65.2 | 4.0900 | 1.0 | 296.0 | 15.3 | 396.90 | 4.98 |

| 1 | 0.02731 | 0.0 | 7.07 | 0.0 | 0.469 | 6.421 | 78.9 | 4.9671 | 2.0 | 242.0 | 17.8 | 396.90 | 9.14 |

| 2 | 0.02729 | 0.0 | 7.07 | 0.0 | 0.469 | 7.185 | 61.1 | 4.9671 | 2.0 | 242.0 | 17.8 | 392.83 | 4.03 |

| 3 | 0.03237 | 0.0 | 2.18 | 0.0 | 0.458 | 6.998 | 45.8 | 6.0622 | 3.0 | 222.0 | 18.7 | 394.63 | 2.94 |

| 4 | 0.06905 | 0.0 | 2.18 | 0.0 | 0.458 | 7.147 | 54.2 | 6.0622 | 3.0 | 222.0 | 18.7 | 396.90 | 5.33 |

(a) For each predictor, fit a simple linear regression model to predict the response. Describe your results. In which of the models is there a statistically significant association between the predictor and the response? Create some plots to back up your assertions.

The p-values for $\beta_1$s suggest that for the model with predictor CHAS, we can not reject the null hypothesis and hence the model is not significant. The plots shown in the below figure suggest the same.

y = df_boston['CRIM']

X = df_boston[['ZN']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['INDUS']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['CHAS']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['NOX']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['RM']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['AGE']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['DIS']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['RAD']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['TAX']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['PTRATIO']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['B']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

X = df_boston[['LSTAT']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

print("\n\n")

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.040

Model: OLS Adj. R-squared: 0.038

Method: Least Squares F-statistic: 20.88

Date: Thu, 06 Sep 2018 Prob (F-statistic): 6.15e-06

Time: 21:37:49 Log-Likelihood: -1795.8

No. Observations: 506 AIC: 3596.

Df Residuals: 504 BIC: 3604.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 4.4292 0.417 10.620 0.000 3.610 5.249

ZN -0.0735 0.016 -4.570 0.000 -0.105 -0.042

==============================================================================

Omnibus: 568.366 Durbin-Watson: 0.862

Prob(Omnibus): 0.000 Jarque-Bera (JB): 32952.356

Skew: 5.270 Prob(JB): 0.00

Kurtosis: 41.103 Cond. No. 28.8

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.164

Model: OLS Adj. R-squared: 0.162

Method: Least Squares F-statistic: 98.58

Date: Thu, 06 Sep 2018 Prob (F-statistic): 2.44e-21

Time: 21:37:49 Log-Likelihood: -1760.9

No. Observations: 506 AIC: 3526.

Df Residuals: 504 BIC: 3534.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -2.0509 0.668 -3.072 0.002 -3.362 -0.739

INDUS 0.5068 0.051 9.929 0.000 0.407 0.607

==============================================================================

Omnibus: 585.528 Durbin-Watson: 0.990

Prob(Omnibus): 0.000 Jarque-Bera (JB): 41469.710

Skew: 5.456 Prob(JB): 0.00

Kurtosis: 45.987 Cond. No. 25.1

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.003

Model: OLS Adj. R-squared: 0.001

Method: Least Squares F-statistic: 1.546

Date: Thu, 06 Sep 2018 Prob (F-statistic): 0.214

Time: 21:37:49 Log-Likelihood: -1805.3

No. Observations: 506 AIC: 3615.

Df Residuals: 504 BIC: 3623.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 3.7232 0.396 9.404 0.000 2.945 4.501

CHAS -1.8715 1.505 -1.243 0.214 -4.829 1.086

==============================================================================

Omnibus: 562.698 Durbin-Watson: 0.822

Prob(Omnibus): 0.000 Jarque-Bera (JB): 30864.755

Skew: 5.205 Prob(JB): 0.00

Kurtosis: 39.818 Cond. No. 3.96

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.174

Model: OLS Adj. R-squared: 0.173

Method: Least Squares F-statistic: 106.4

Date: Thu, 06 Sep 2018 Prob (F-statistic): 9.16e-23

Time: 21:37:50 Log-Likelihood: -1757.6

No. Observations: 506 AIC: 3519.

Df Residuals: 504 BIC: 3528.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -13.5881 1.702 -7.986 0.000 -16.931 -10.245

NOX 30.9753 3.003 10.315 0.000 25.076 36.875

==============================================================================

Omnibus: 591.496 Durbin-Watson: 0.994

Prob(Omnibus): 0.000 Jarque-Bera (JB): 42994.381

Skew: 5.544 Prob(JB): 0.00

Kurtosis: 46.776 Cond. No. 11.3

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.048

Model: OLS Adj. R-squared: 0.046

Method: Least Squares F-statistic: 25.62

Date: Thu, 06 Sep 2018 Prob (F-statistic): 5.84e-07

Time: 21:37:50 Log-Likelihood: -1793.5

No. Observations: 506 AIC: 3591.

Df Residuals: 504 BIC: 3600.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 20.5060 3.362 6.099 0.000 13.901 27.111

RM -2.6910 0.532 -5.062 0.000 -3.736 -1.646

==============================================================================

Omnibus: 576.890 Durbin-Watson: 0.883

Prob(Omnibus): 0.000 Jarque-Bera (JB): 36966.825

Skew: 5.361 Prob(JB): 0.00

Kurtosis: 43.477 Cond. No. 58.4

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.123

Model: OLS Adj. R-squared: 0.121

Method: Least Squares F-statistic: 70.72

Date: Thu, 06 Sep 2018 Prob (F-statistic): 4.26e-16

Time: 21:37:50 Log-Likelihood: -1772.9

No. Observations: 506 AIC: 3550.

Df Residuals: 504 BIC: 3558.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -3.7527 0.944 -3.974 0.000 -5.608 -1.898

AGE 0.1071 0.013 8.409 0.000 0.082 0.132

==============================================================================

Omnibus: 575.090 Durbin-Watson: 0.960

Prob(Omnibus): 0.000 Jarque-Bera (JB): 36851.412

Skew: 5.331 Prob(JB): 0.00

Kurtosis: 43.426 Cond. No. 195.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.143

Model: OLS Adj. R-squared: 0.141

Method: Least Squares F-statistic: 83.97

Date: Thu, 06 Sep 2018 Prob (F-statistic): 1.27e-18

Time: 21:37:50 Log-Likelihood: -1767.1

No. Observations: 506 AIC: 3538.

Df Residuals: 504 BIC: 3547.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 9.4489 0.731 12.934 0.000 8.014 10.884

DIS -1.5428 0.168 -9.163 0.000 -1.874 -1.212

==============================================================================

Omnibus: 577.090 Durbin-Watson: 0.957

Prob(Omnibus): 0.000 Jarque-Bera (JB): 37542.100

Skew: 5.357 Prob(JB): 0.00

Kurtosis: 43.815 Cond. No. 9.32

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.387

Model: OLS Adj. R-squared: 0.386

Method: Least Squares F-statistic: 318.1

Date: Thu, 06 Sep 2018 Prob (F-statistic): 1.62e-55

Time: 21:37:50 Log-Likelihood: -1682.3

No. Observations: 506 AIC: 3369.

Df Residuals: 504 BIC: 3377.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -2.2709 0.445 -5.105 0.000 -3.145 -1.397

RAD 0.6141 0.034 17.835 0.000 0.546 0.682

==============================================================================

Omnibus: 654.232 Durbin-Watson: 1.336

Prob(Omnibus): 0.000 Jarque-Bera (JB): 74327.568

Skew: 6.441 Prob(JB): 0.00

Kurtosis: 60.961 Cond. No. 19.2

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.336

Model: OLS Adj. R-squared: 0.335

Method: Least Squares F-statistic: 254.9

Date: Thu, 06 Sep 2018 Prob (F-statistic): 9.76e-47

Time: 21:37:50 Log-Likelihood: -1702.5

No. Observations: 506 AIC: 3409.

Df Residuals: 504 BIC: 3418.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -8.4748 0.818 -10.365 0.000 -10.081 -6.868

TAX 0.0296 0.002 15.966 0.000 0.026 0.033

==============================================================================

Omnibus: 634.003 Durbin-Watson: 1.252

Prob(Omnibus): 0.000 Jarque-Bera (JB): 63141.063

Skew: 6.134 Prob(JB): 0.00

Kurtosis: 56.332 Cond. No. 1.16e+03

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.16e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.083

Model: OLS Adj. R-squared: 0.081

Method: Least Squares F-statistic: 45.67

Date: Thu, 06 Sep 2018 Prob (F-statistic): 3.88e-11

Time: 21:37:50 Log-Likelihood: -1784.1

No. Observations: 506 AIC: 3572.

Df Residuals: 504 BIC: 3581.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -17.5307 3.147 -5.570 0.000 -23.714 -11.347

PTRATIO 1.1446 0.169 6.758 0.000 0.812 1.477

==============================================================================

Omnibus: 568.808 Durbin-Watson: 0.909

Prob(Omnibus): 0.000 Jarque-Bera (JB): 34373.378

Skew: 5.256 Prob(JB): 0.00

Kurtosis: 41.985 Cond. No. 160.

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.142

Model: OLS Adj. R-squared: 0.141

Method: Least Squares F-statistic: 83.69

Date: Thu, 06 Sep 2018 Prob (F-statistic): 1.43e-18

Time: 21:37:50 Log-Likelihood: -1767.2

No. Observations: 506 AIC: 3538.

Df Residuals: 504 BIC: 3547.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 16.2680 1.430 11.376 0.000 13.458 19.078

B -0.0355 0.004 -9.148 0.000 -0.043 -0.028

==============================================================================

Omnibus: 591.626 Durbin-Watson: 1.001

Prob(Omnibus): 0.000 Jarque-Bera (JB): 43282.465

Skew: 5.543 Prob(JB): 0.00

Kurtosis: 46.932 Cond. No. 1.49e+03

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.49e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.205

Model: OLS Adj. R-squared: 0.203

Method: Least Squares F-statistic: 129.6

Date: Thu, 06 Sep 2018 Prob (F-statistic): 7.12e-27

Time: 21:37:50 Log-Likelihood: -1748.2

No. Observations: 506 AIC: 3500.

Df Residuals: 504 BIC: 3509.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const -3.2946 0.695 -4.742 0.000 -4.660 -1.930

LSTAT 0.5444 0.048 11.383 0.000 0.450 0.638

==============================================================================

Omnibus: 600.766 Durbin-Watson: 1.184

Prob(Omnibus): 0.000 Jarque-Bera (JB): 49637.173

Skew: 5.638 Prob(JB): 0.00

Kurtosis: 50.193 Cond. No. 29.7

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

sns.pairplot(df_boston, y_vars=['CRIM'], x_vars=['NOX', 'RM', 'AGE', 'DIS', 'LSTAT', 'CHAS'])

<seaborn.axisgrid.PairGrid at 0x11bb509e8>

(b) Fit a multiple regression model to predict the response using all of the predictors. Describe your results. For which predictors can we reject the null hypothesis H0 : βj = 0?

For the predictors: DIS, RAD, BLACK, LSTAT, we can reject the null hypothesis.

Y = df_boston['CRIM']

X = df_boston[['ZN', 'INDUS', 'CHAS', 'NOX', 'RM', 'AGE', 'DIS', 'RAD', 'TAX', 'PTRATIO', 'B', 'LSTAT']]

X = sm.add_constant(X, prepend=True)

model = sm.OLS(y, X)

result = model.fit()

print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: CRIM R-squared: 0.436

Model: OLS Adj. R-squared: 0.422

Method: Least Squares F-statistic: 31.77

Date: Thu, 06 Sep 2018 Prob (F-statistic): 6.16e-54

Time: 21:37:50 Log-Likelihood: -1661.2

No. Observations: 506 AIC: 3348.

Df Residuals: 493 BIC: 3403.

Df Model: 12

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 10.3701 7.012 1.479 0.140 -3.408 24.148

ZN 0.0365 0.019 1.936 0.053 -0.001 0.073

INDUS -0.0672 0.085 -0.794 0.428 -0.233 0.099

CHAS -1.3049 1.185 -1.101 0.271 -3.633 1.023

NOX -7.2552 5.250 -1.382 0.168 -17.570 3.060

RM -0.3851 0.575 -0.670 0.503 -1.515 0.745

AGE 0.0019 0.018 0.105 0.917 -0.034 0.038

DIS -0.7163 0.273 -2.626 0.009 -1.252 -0.180

RAD 0.5395 0.088 6.128 0.000 0.366 0.712

TAX -0.0013 0.005 -0.254 0.799 -0.011 0.009

PTRATIO -0.0907 0.180 -0.504 0.615 -0.445 0.263

B -0.0089 0.004 -2.428 0.016 -0.016 -0.002

LSTAT 0.2309 0.069 3.346 0.001 0.095 0.366

==============================================================================

Omnibus: 680.813 Durbin-Watson: 1.507

Prob(Omnibus): 0.000 Jarque-Bera (JB): 94712.935

Skew: 6.846 Prob(JB): 0.00

Kurtosis: 68.611 Cond. No. 1.51e+04

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.51e+04. This might indicate that there are

strong multicollinearity or other numerical problems.